How Palus Builds Suitable Treasury Strategies for Its Customers

After fundraising, you have a massive pile of cash and a long runway. That cash is both a responsibility and an opportunity: a lot of money that needs to be managed appropriately, but also a chance to get safe, free money for your company if you do it right.

Why other treasury products get it wrong

Most treasury products take a one-size-fits-all approach to your company's cash: every dollar gets swept into the same money market fund, whether you need it next week or next year. The product never considers how your business actually uses the money. In fact, these products intentionally avoid giving you any financial advice about how to manage your cash.

A money market fund is a useful tool, but like any tool it fits some situations and not others. It's an ultra-short-term instrument: designed to be super liquid for cash you need next week, but explicitly not meant for cash you won't touch for a long time. You pay a lot for that liquidity without your money being any safer, which is why money market funds are not suitable long-term cash.

Thankfully, there are best practices and industry standards about how to think about cash, and which investments are suitable for which segments of your company's treasury. These are the guidelines Palus follows when we design treasury strategies for our customers.

Suitability is about timing, not risk

As fiduciaries, when we allocate customers' treasuries, we are legally required to ensure their money is always invested in suitable assets aligned with their financial profile.

Of course, priority #1 for a startup's treasury is not losing money. This means it should always be invested super conservatively, whether in checking accounts, money market funds, or anything else. So suitability comes down to one question: does where the money sits match when you'll need it? The question is about timing, not risk: the expected time horizon of the investment, and how quickly you need to access the money.

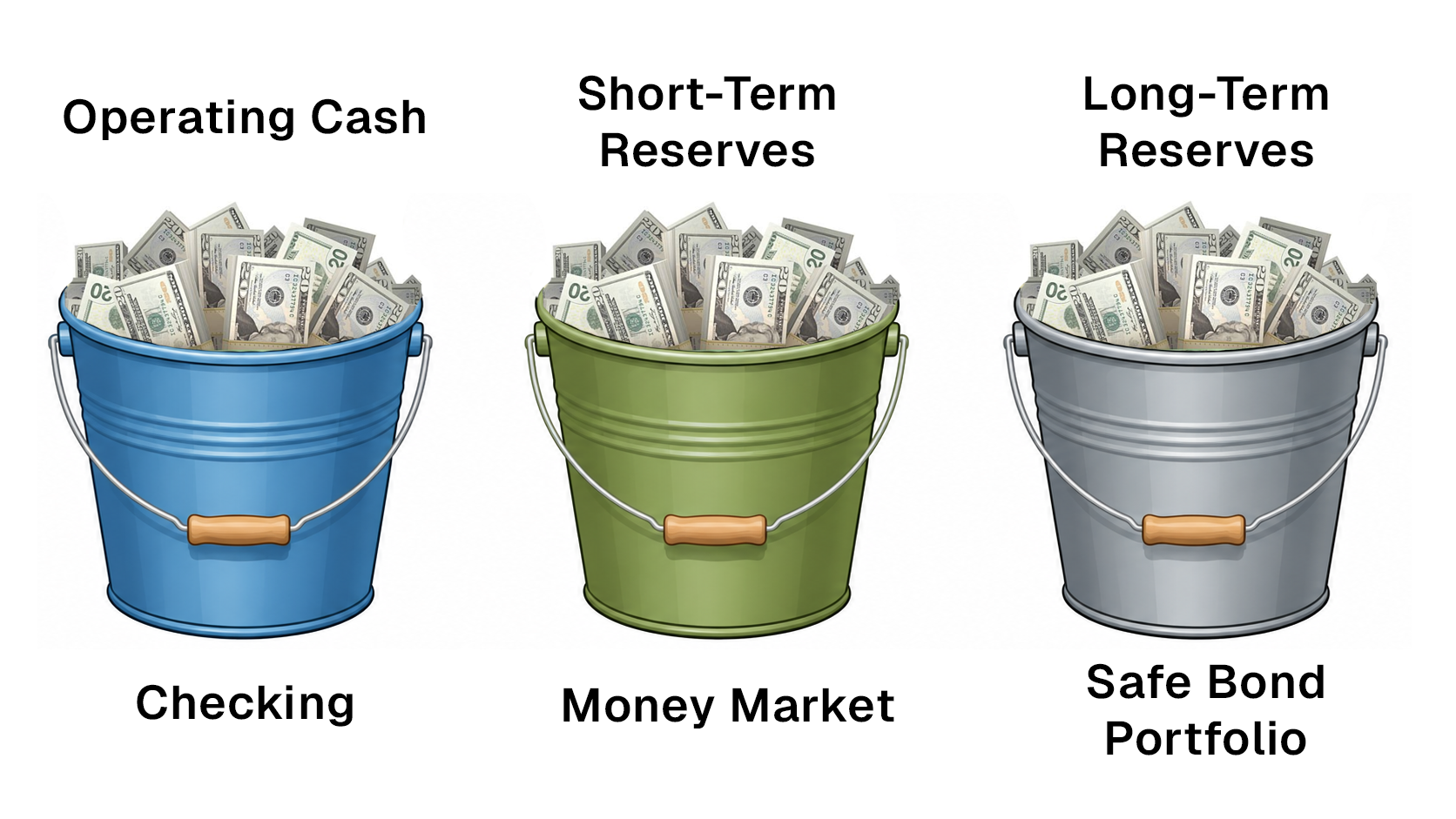

We start by sorting cash based on when you'll need it

The National Venture Capital Association (NVCA), an industry group which your investors are almost certainly part of, has published guidelines on how startups should manage their treasury. NVCA recommends sorting cash into a few simple buckets by time horizon:

- Operating cash for the normal ins and outs of the business, needed on demand.

- Reserve cash set aside for near-future needs, available within a day or two.

- Strategic cash with a roughly 1-year time horizon, available on longer notice.

The reason to sort is that a longer horizon opens up options the overnight bucket doesn't have. Cash you won't need for a while can be put to better use at the same level of risk, because time is what makes that possible. The benefits come from time horizon, not extra risk.

What NVCA recommends for long-term cash

For reserve and strategic cash, NVCA recommends safe, government-backed securities with maturity and duration timed to when you need the cash. It's a conservative, well-established approach and it's the foundation our bond strategies are built on. The aim is straightforward: keep the money safe and available when you'll need it, and stop treating long-horizon cash the same as short.

How we build suitable portfolios for startups

We tailor each customer's strategy to its financial profile, so the result is suitable for them specifically. We account for the company's assets; burn, revenue, and expected changes in both; upcoming fundraising plans; customer preferences; and any other key details that may impact suitability and strategy.

That being said, long-term reserves of most startups point in a similar direction, since most want the same things from that money. The key requirements for long-term reserves are typically:

- Protect your money above all else

- Plan as if you won't need the money for several months or longer

- You can tolerate reasonable lockup periods

We build around that with conservative portfolios of government-backed bonds. Holdings are chosen to protect your investment, line up duration with when the company expects to use the money, and allow up to 3 days to cash out (much, much shorter than the time horizon of this cash).

The approach is consistent across clients because their goals are consistent, but the specifics for how much to allocate where are set to each company's own plans and needs.

In conclusion

Building and managing a treasury strategy takes work, and it's far from a top priority for most founders and early-stage finance leaders. That's why Palus takes it off your plate and handles it all for you.

As a fiduciary, we have a legal requirement to ensure above all else that your money is invested suitably. Your money is always handled the way you, your investors, and NVCA expect a good steward to handle it.

If you'd like to learn more about our treasury strategies, advisory services, or startup finance generally, please book a call.

This material is for informational purposes only and is not investment advice. Draft pending compliance review.