You Just Raised Your Seed Round. Here's What to Do With the Cash.

You've finally closed your seed round. The wires hit. There's more money in your company's bank account than you've ever seen. Congratulations!

But now what?

You probably just spent weeks fundraising and letting other responsibilities pile up, and you can't wait to go back to building. But the decision you make (or don't make) about where that cash sits for the next 18–24 months can quietly cost you hundreds of thousands of dollars a year. And the default option, leaving it all in your checking account, is almost certainly the wrong one.

Here's how to think about treasury management after a raise, even if you never want to think about it again.

The Cost of Doing Nothing

Let's say you raised $5M. If that cash sits in a standard checking account earning close to 0%, you're leaving real money on the table every single month. Even 1% yield is $50k a year, for free. At 5%, it's $250k. The difference between 0% and 5% is:

- A free senior engineer

- An SF freeway billboard

- Months of runway

- A dent in your dilution

The math is straightforward, and yet most seed-stage founders don't act on it. Not because they're bad with money, but because they're busy building a company and treasury management feels like something only Fortune 500 CFOs worry about.

But here's the thing: this is a problem you can solve in five minutes and never think about again. Those might be the most lucrative five minutes of your career as an early-stage founder.

And every month you put it off, you're quietly wasting thousands of dollars.

Step 1: Figure Out Your Cash Buckets

Not all of your cash has the same job. The single most important thing you can do is separate your funds by time horizon:

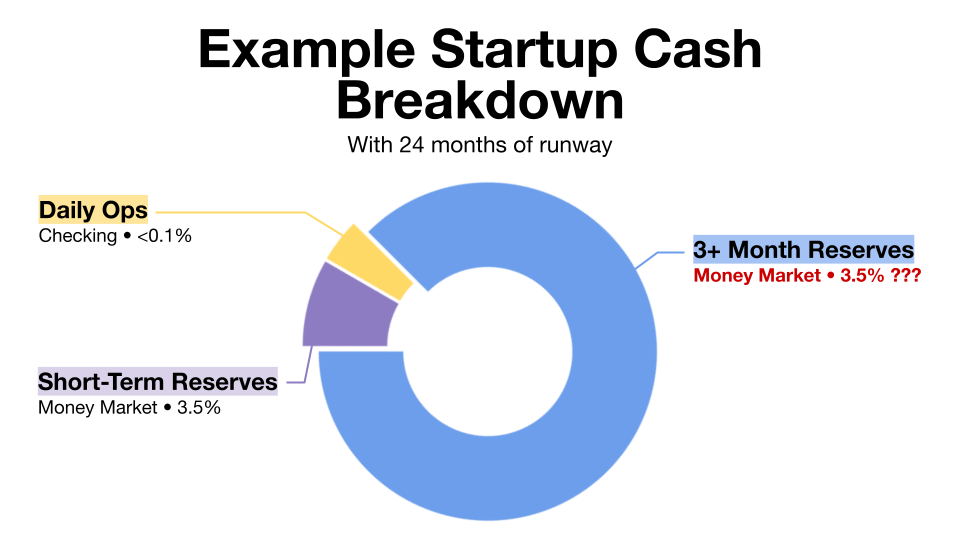

Operating cash (~1 month of runway). This is the money you'll actually spend soon on things like payroll, rent, and software. Keep this liquid and accessible in your primary checking account. You need instant access to this money, and yield doesn't matter much here.

You always want enough in your checking account to cover immediate expenses, but not too much more, since there's opportunity cost in yield.

Short-term reserves (1–3 months out). Cash you want easy access to, but not immediately. How you handle this depends on your company, burn rate, revenue, etc. Some founders use a high-yield savings account or money market fund, and others don't bother with a separate bucket here and split the money between their checking account and long-term treasury. No single right answer.

Long-term treasury (3+ months out). The portion of your raise you won't touch for a while. This is where yield can make a real difference. Because you have a longer time horizon, you can tolerate slightly less liquidity in exchange for meaningfully better returns. This is where most startups leave the most money on the table, because they treat it the same as their operating cash.

The key insight is that a dollar you won't spend for 12 months shouldn't sit in the same place as a dollar you need for next week's payroll. Matching your investment strategy to your actual cash flow timeline is exactly what institutional treasury teams do, and it's how you earn more without taking on more risk.

Step 2: Don't Keep Everything in One Place

When you opened your Mercury or Brex account during YC, it made sense to keep things simple. One bank, one account, move fast. But after a raise, consolidating all your cash with a single provider creates two problems:

First, concentration risk. FDIC coverage is mostly a solved problem now, since every major startup bank offers a sweep network. But if your bank itself runs into trouble, having all your cash in one place can be a serious problem. Companies that banked exclusively with SVB in 2023 know this firsthand: when things went sideways, companies with no diversification were scrambling to make payroll.

Likewise, some money market funds have occasionally gated redemptions or charged withdrawal fees during stress periods, so diversifying across different funds and asset types is a good thing.

Second, yield opportunity cost. Your bank's treasury product is almost certainly a money market sweep earning around 3.5%. That's fine for short-term cash, but for long-term reserves it literally leaves risk-free yield on the table (the reason why is a bit finance-y; you can look up "bond duration matching" to learn about it, or we'll publish a deeper dive on how it works soon). Long story short, most treasury products on the market aren't actually designed to handle long-term cash efficiently.

This doesn't mean you need five bank accounts and a spreadsheet, but it means your operating account and your treasury strategy shouldn't be the same product.

Caption: this is how most treasury products (except for Palus!) treat your cash, treating your long-term reserves the same as your short-term. Don't do this.

Step 3: Automate It and Move On

The best treasury strategy is one you don't have to manage. If you're a seed-stage founder spending time manually moving money between accounts, you're doing it wrong.

Look for solutions that let you set up automated transfers from your yield-bearing treasury accounts back to your checking account. This can be on a schedule, or when your checking falls below a certain threshold. The goal is a system where cash earns the most when it should, and flows back to your operating account when you need it, without you logging in or thinking about it.

You have a company to build. Treasury management should run in the background.

What We Built at Palus

This is exactly the problem we built Palus to solve. We're a treasury management platform designed specifically for recently-funded startups.

Palus is built specifically for your long-term cash, the bucket that most startup treasury products handle poorly. Our founders used to build treasury strategies for Fortune 500 companies, and started Palus to make those same strategies available to startups.

Our portfolio invests in floating-rate agency MBS, the same asset class that Fortune 500 treasury teams have used for decades, but that's traditionally been unavailable to smaller companies. Instead of the ~3.5% yield you'd get from Mercury, Rho, or Brex, our users earn up to 5% – roughly 40% more yield, without taking on additional risk.

A few things that matter for founders:

Your cash is always accessible. You can pull funds out within 3 business days, and you can set up auto-transfers from Palus back to your checking account so cash is there when you need it.

You keep your existing bank. Palus connects to your current account. You don't have to switch banks or change your payment workflows. Setup takes less than five minutes.

Institutional-grade infrastructure. Your capital is held with Alpaca, an SEC-licensed custodian, and insured up to $75M. Our floating-rate MBS portfolio is managed by Regan Capital, the largest investment manager for this asset class in the country. That's a level of institutional infrastructure that most startup yield products don't offer.

It's fully automated. No spreadsheets, no manual rebalancing, no "treasury management" on your to-do list. Quickly set up automated transfer rules when you open your account and never think about it again.

We designed Palus so that setup takes less than five minutes (quicker than reading this blog post).

For a startup that raised $5M, the difference between a typical 3.5% treasury product and Palus is roughly $75K a year. That's an extra employee, a marketing campaign, or another month of runway when you need it most.

The TL;DR

After your raise, keep about a month of operating expenses in checking and put the rest to work earning yield. Don't treat all your cash the same: segment it by when you'll actually need it. Diversify across providers and asset classes instead of parking everything with your primary bank. Automate the whole thing so you never think about it.

And if you want the short version of all of that: just set up Palus and get back to building.